At the 21st annual WBS Quantitative Finance Conference in Palermo (September 2025), several presentations focused on computing autocallable Greeks, highlighting the active research in this space. We contributed a practical, production-ready implementation with concrete cost savings, including a complete open-source methodology.

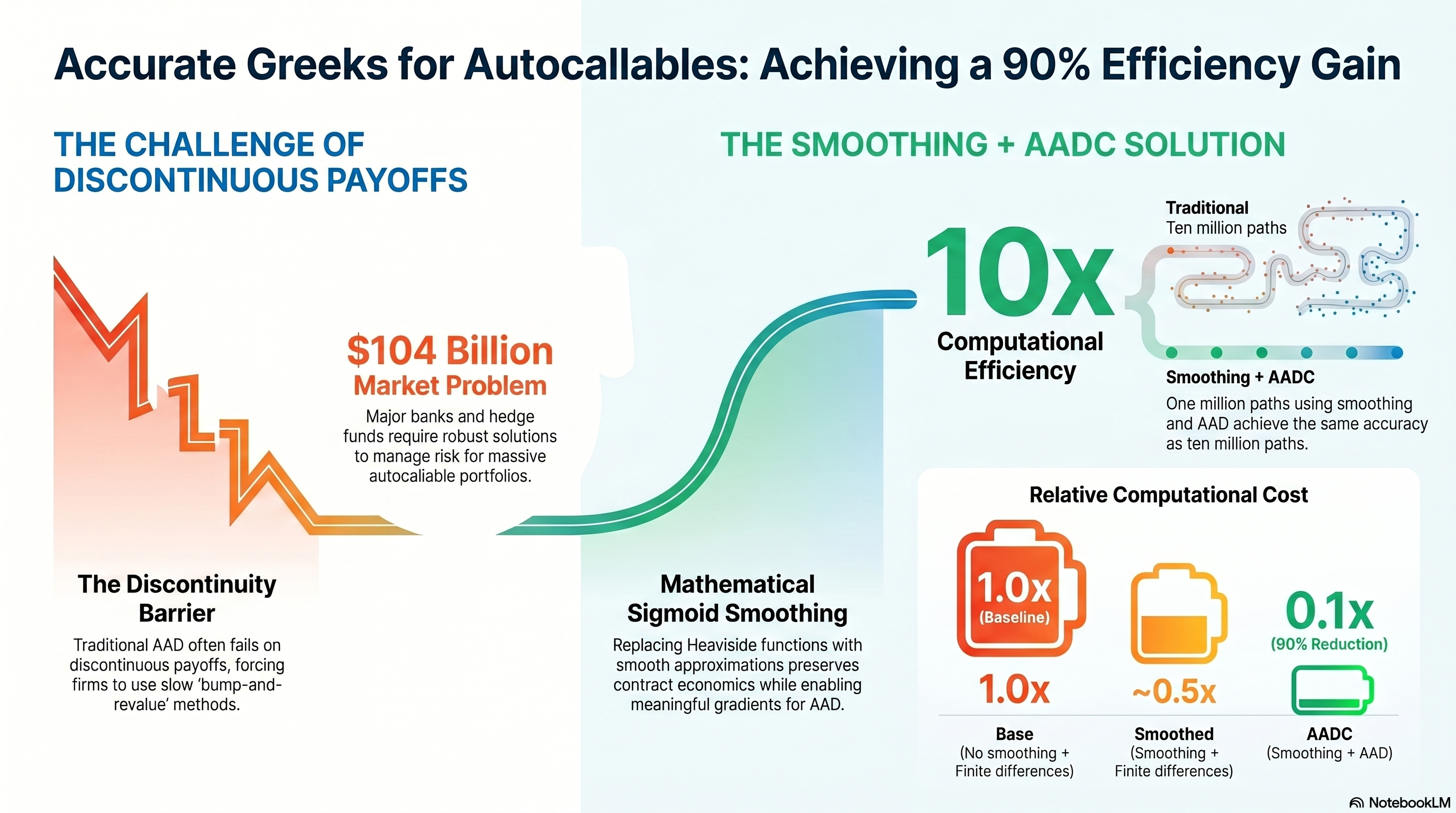

Conference discussions validated the urgent need for robust solutions for the $104B autocallable market, with participants ranging from major banks, specialized boutiques, and hedge funds, all wrestling with the same Greeks calculation challenges.

The problem

Despite AAD adoption by ~20% of Tier 1 banks, the debate over computing autocallable Greeks remains unsettled. A vocal contingent argues that “AAD doesn’t work for discontinuous payoffs,” while others persist with expensive bump-and-revalue approaches.

Bump-and-revalue leaves you stuck with 10M+ paths for stable correlation Greeks, noisy results OTM, and uncertain bump sizes introducing error rates of up to 10%.

Pathwise AAD on its own requires continuous payoffs, and standard application to digitals yields zero gradients almost everywhere. However, dismissing AAD entirely would mean losing the methodology’s significant efficiency gains.

The solution: Smoothing + AAD

The key insight is that you don’t need to work with the discontinuous payoff directly. Replace Heaviside functions with smooth sigmoid approximations that preserve contract economics:

contLess(a, b, h) =

h = 0: 1{a < b}

h > 0: ½(((b-a)/(0.02h))/√(1+((b-a)/(0.02h))²) + 1)Properties that matter:

- Area under the smoothed curve ≈ original digital (quantifiable price difference)

- Enables meaningful gradients for AAD

- Tunable parameter for accuracy/stability tradeoff

- Provable convergence as

Three methods benchmarked

We benchmarked on a Phoenix Autocallable (2-asset worst-of, quarterly observations):

| Method | Description | Relative Cost |

|---|---|---|

| Base | No smoothing + finite differences | 1.0× (baseline) |

| Smoothed | Smoothing + finite differences | ~0.5× |

| AADC | Smoothing + AAD | 0.1× (90% reduction) |

The key finding: 1M paths with smoothing + AAD achieves the same accuracy as 10M paths with bump-and-revalue. That’s a 90% reduction in computational cost.

Correlation Greeks — traditionally the noisiest and most expensive — become stable at a fraction of the cost.

Open source

Complete C++ implementation available at github.com/matlogica/QuantBench.

Presented at WBS Quantitative Finance Conference, Palermo, September 2025. Implemented using AADC, a commercial adjoint AD compiler (matlogica.com).

Frequently Asked Questions

How does AAD work for autocallable Greeks?

By combining mathematical smoothing with Automatic Adjoint Differentiation, we achieve 90% computational cost reduction while maintaining accuracy for autocallable structured products. Smoothing replaces Heaviside functions with sigmoid approximations that preserve contract economics and enable meaningful AAD gradients.

What is the performance improvement with smoothing + AAD?

1M paths with smoothing+AAD achieves comparable or better accuracy than 10M paths using traditional bump-and-revalue methods, representing a 90% reduction in computational cost and orders of magnitude improvement in efficiency.

Can AAD handle discontinuous payoffs like autocallables?

Standard pathwise AAD cannot directly handle discontinuous payoffs (yields zero gradients). However, by applying mathematical smoothing to convert digitals into smooth sigmoid approximations, AAD becomes highly effective while maintaining accuracy and enabling massive computational savings.

How do you validate that smoothed payoffs converge correctly?

The area difference between smoothed and actual digital is mathematically quantifiable. Convoluting with the density function gives measurable price deviation. In practice, relative error is small for material payoffs and negligible when digital value itself is small.